The Offshore Dollar is Being Left Out to Dry

Don’t Get Caught Holding the Last Eurodollar in a Stablecoin World

The election of November 2024 will go down as a critical fork in the road in the monetary history of the United States. Its result not only established the future course and structure of the U.S. dollar that the American economy and its cooperative trade partners will transact on for the intermediate future. It also reshaped how domestic institutions will respond as future crises in the global financial system materialize. This has major ramifications for financial markets and investors going forward. Unfortunately, many still operate under assumptions and old habits that only hold true in a world that is now gone with the wind.

“Perhaps—I want the old days back again and they’ll never come back, and I am haunted by the memory of them and of the world falling about my ears.”

Margaret Mitchell, Gone with the Wind

The overwhelming majority of finance professionals in their seats today came of age during the era of Fed Dominance that spanned the Greenspan, Bernanke, Yellen, and Powell tenures across nearly four decades. In this epoch, unfettered dollar-denominated credit expansion was systematically encouraged both in the U.S. and abroad1, with the Fed’s monetary policy serving as the primary lever used to prop up the ever-increasing pile of debt from below2. Every time global economic growth slowed and crisis surfaced, a version of the same copypasta policy prescription was deployed to ward off the threat of instability under the monetary structure of the prior era: legislators flushed the greasy pipes of Washington D.C. with fiscal spending packages (typically in an amount exceeding the preceding crisis by an order of magnitude), while the central bank lowered interest rates and increasingly utilized its balance sheet to purchase excess debt inside the financial system (“QE”). Those paying attention learned to correctly anticipate this policy response from the system as a key driver of investment returns and did well for themselves.

To work, this model required the subservience of the U.S. Treasury: the public sector had to provide its “risk-free” debt in ever bottomless quantities as the ultimate collateral to the system. All the fiscal spending and QE in recent decades arise from this fact: the one-way proliferation of credit that this global dollar system ran on imperatively required the U.S. government to run up and blow out its own tally of outstanding debt. So, from a different vantage point, labeling this period we’re leaving behind as the era of Treasury Subservience would accurately describe the other side of the same coin to the Fed’s dominance.

The Treasury’s mounting debt problem under this system never went without notice. The national debt clock in downtown Manhattan has drawn public attention to the nation’s open tab since 1989, while several politicians have made the national debt issue a core feature of their unsuccessful presidential campaigns. The problem was recognized in real time, but none of these efforts had any power to address the problem’s root cause that was structural in nature. The ballooning national debt, a direct output of the structural imbalances required by the system, can only be resolved through structural reform to the monetary system itself. That reform is already well underway, most of us just couldn’t recognize it on first impression.

With the 2024 election result, and the cooperation of Congress and the President, Treasury Secretary Scott Bessent has led the groundwork preparation for the “stablecoin” dollar – the new structure riding the technological wave that Bitcoin’s arrival in 2008 first ushered in3. That dollar will eventually supplant and replace the offshore credit dollar of the era we’re leaving behind. With the confirmation of Kevin Warsh as new Fed chair this May, all the pieces are now in place. The era of Treasury Supremacy has arrived. Over the next few years, an entirely different world is set to emerge as the most influential period in the handoff between these two dollars takes place. Investors’ habits and instincts learned in the prior era may no longer be dependable in a new era where the system has fundamentally changed.

Someday we’ll all just call these stablecoins dollars

While the underlying “crypto” rails that support the stablecoin dollar are new, what they are providing is conceptually simple: instead of a dollar that takes the form of a liability claim against a financial intermediary’s balance sheet, the stablecoin dollar takes an asset form as a Treasury Bill melded into a shape that can be transmitted over the Internet. In the old framework, the liability dollar is transferred (“moves”) via messages on the SWIFT network that direct accounting entries on balance sheets located across jurisdictions around the world — outside of the Fed and Treasury’s regulatory purview (hence the term “offshore”). Now competing head to head on that same global field of competition, the key feature of the stablecoin dollar is that there is now a thing that is itself separable within the transaction where a dollar moves through the financial system from counterparty A to counterparty B.

Banks and financial institutions will now have something to move when they transact, not just a bilateral reconciliation of accounting entries to update their ledgers with nothing to latch onto in between. That distinction might sound minor but represents a massive change from the old system. Now, rather than the Fed and Treasury being held hostage to reliquefy financial institutions any time the overleveraged liability dollar system comes under duress in a crisis, private savings in the dollar have an exit from the liability cascade. People and businesses now have access to an asset dollar that is separable and sits a step removed from the system leverage dynamic.

This is an important development decades in the making. The private sector has not had a way to protect its savings in the dollar from yield-seeking risk in the debt-based financial system ever since policymakers abandoned the dollar’s redeemability into precious metals in 19684 and 19715. This product feature is something the private sector will naturally come to realize it prefers over the incumbent offering one crisis at a time. As future financial crises unfold, these panics will provide a tailwind into the stablecoin dollar and increase its market share against the incumbent framework. With private savings safely out of the line of fire, the balance of monetary policy then accordingly shifts away from Fed monetization of excess system credit onto its balance sheet and back to its classic lender of last resort function. As adoption of the asset dollar pushes out the old, Treasury funding steers towards short-term borrowing in the bills market that will increasingly find its way flowing into its tokenized form as stablecoin dollars.

Notice there is a “pulling itself up by its own bootstraps” going on with the stablecoin dollar’s ultimate backing: the asset dollar itself derives its substance from a Treasury Bill IOU that wholly exists within the realm of the legacy credit dollar that’s being supplanted. That’s a feature, not a bug. As stablecoin dollars are integrated into the commercial banking systems of the United States and its trade partners, the old debt from the prior monetary paradigm gradually collapses onto the new. What happens when the old liability dollar dries up and funding capacity in the stablecoin market outgrows these IOUs? The self-referencing nature of the stablecoin dollar suggests it is not the destination. It is a monetary shunt that bridges us from the past to the future. That bridge will be crossed when it arrives, but history suggests an eventual repeg of the dollar to a base money commodity in the hands of the private sector as the most probable outcome.

In the meantime, these tailwinds will accelerate the breakdown and deleveraging of the old trade and financial system that is already underway. Trade relationships will be redrawn in the years ahead, as the events of early 2026 in Venezuela and Iran have already begun to foretell. On the other side of this process, the loser will be the holders of purchasing power stored in the liability dollars of the legacy offshore system whose best days are in the rearview mirror.

There are people alive today who have lived through a transition like this before

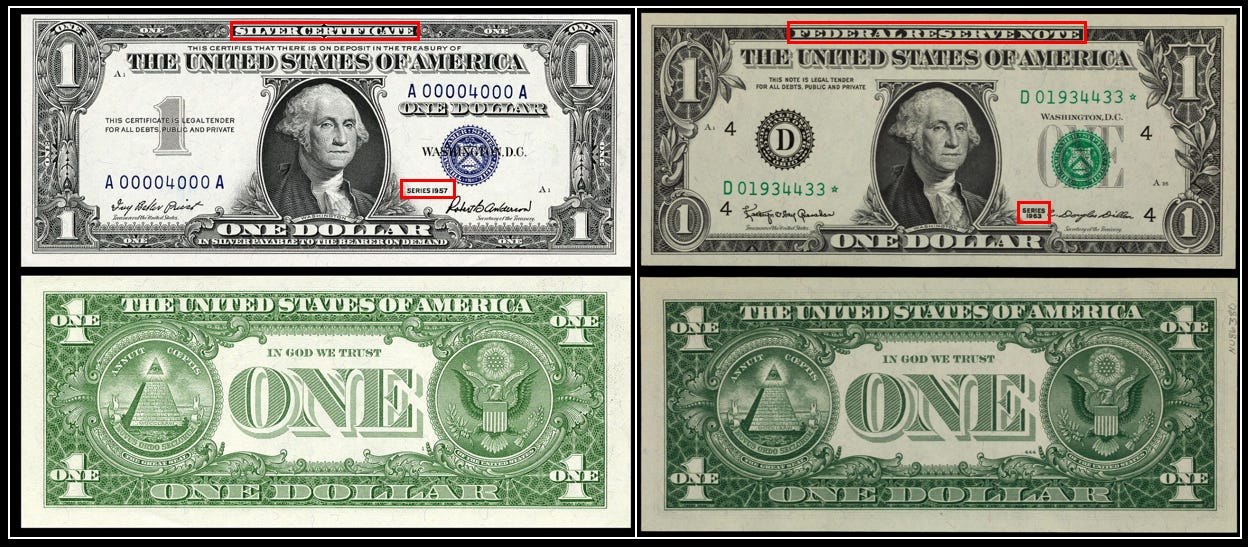

Many Americans alive today have already experienced a structural transition from one dollar to the next. In the opposite direction of travel from the transition going on in the present, a liability dollar replaced an asset dollar incumbent during the 1960s when two paper dollars briefly circulated in the American economy at the same time: silver certificates issued by the Treasury, redeemable into bullion until its exchange window closed for good in 1968, and Federal Reserve Notes that first appeared without the language “will pay to the bearer on demand” in 1963.

To many the difference between these paper notes looked unremarkable, most easily differentiated by the color of their Treasury seal and serial number (blue for the silver certificates, green for Federal Reserve notes) and obligation clauses6. Harkening back to the greenback of the Civil War era, they shared an identical reverse featuring monochromatic green artwork that is still featured on paper notes in circulation today7.

While most people exchanged the notes at equal value and otherwise carried on with economic life during that time, a few sharp individuals saw what was happening and profited handsomely from the dollar transition. Henry Jarecki made a legendary fortune advertising in newspapers to buy the silver certificates from the public, which he then redeemed into bullion and sold into market at a profit8. For those who see it, a similar opportunity window for profitable conversion between two dollars is opening today. As the U.S. Treasury’s funding plan reduces the maturity profile of its public debt, the makeup of the liability dollars of the legacy system are increasingly shifting into discounted Treasury Bills. A portion of this bill issuance will find its way into reserves backing the issuance of the new asset dollars from a stablecoin issuer.

As trade partners with the United States integrate these stablecoin dollars into their banking systems, purchasing power gravitates towards the new dollar and fades from the old. With some estimates of outstanding debt claims tied up in these old liability dollars exceeding $350 trillion9, that glut of purchasing power up for grabs during this dollar transition may well end up dwarfing the spoils of arbitrage captured by the speculators who captured a sizable share of the value transferred when the dollar’s silver peg was broken almost six decades ago. For everybody else, people will adapt and life will go on.

Japan is the next operational theater

In June, Japan will begin to allow stablecoin dollars issued by foreign domiciled trusts to serve as a legal payment method within its domestic banking system10. This decision coincides with the country’s own sovereign debt market and currency veering towards their own breaking point under the old liability dollar system, an inevitable stumbling block arising from the Japanese economy’s dependence on energy imports from global producers that must be paid in dollars. Under the status quo, Japan’s banking system relies on access to the global foreign exchange market to access the dollars that it needs in order to import the commodities its economy depends on. Going forward, every dollar it can shift away from the liability dollar to an asset dollar allows the Japanese Yen to bypass the added tolls of bid-ask spreads, volatility, and hedging costs it pays to foreign exchange middlemen just to access the dollar it has always been ultimately after: the lowest risk dollars in the system that take the form of onshore Fed liabilities or Treasury bill claims. The stablecoin cuts what was formerly a two hop trip down to one.

For settlement of bilateral trade between the U.S. and Japan that exceeds $200 billion annually11, look for the stablecoin dollar to gain market share as the underlying capacity of this market continues to grow. And as Japan’s onboarding increases the incentive for future adopters, this monetary restructuring looks like a flywheel gathering energy. As trade and financial relationships reorder around this dollar transition taking place, marginal dollar supply in this new world depends increasingly less on central bank balance sheet expansion and more on resource production and cross-border value-added trade.

For better or worse, the money printer has been handed over to the Treasury. Expect volatility to come hand in hand with this change, but likely in ways that differ from what the prior era taught investors to expect. New lessons will be learned, but we’ll survive. After all, tomorrow is another day.

To be continued …

Often referred to as the “Eurodollar” or “offshore dollar” market. For a concise overview of the market’s definition, history, participants, and role in U.S. dollar funding, see Federal Reserve Bank of New York, Liberty Street Economics, “The Eurodollar Market in the United States,” May 26, 2015.

Traders have infamously nicknamed their implied backstop during this era after the Fed chairs – i.e. the “Greenspan Put”, “Bernanke Put”, “Yellen Put”, and “Powell Put”. Those caught off guard by the fact that the game has changed may find out they’re due for a “Warsh” rinsing.

Nakamoto, Satoshi. “Bitcoin: A Peer-to-Peer Electronic Cash System.” 2008. Available at https://bitcoin.org/bitcoin.pdf.

The U.S. Treasury ended the redeemability of its silver certificates mostly used by the private sector on June 24, 1968, and …

Richard Nixon formally closed the dollar’s redeemability into gold for financial institutions operating in cross-border capital markets on August 15, 1971.

Silver certificates promised that a stated number of dollars in silver was “payable to the bearer on demand,” whereas the 1963 Federal Reserve Note dropped any metal‑payment promise and kept only generic legal‑tender language for “all debts, public and private.”

Nearly all U.S. money in the form of paper notes has inherited the green reverse from the Civil War–era “greenbacks,” the first nationally issued legal-tender notes whose backs were printed in green ink.

Henry Sender, “From Healing to Making a (Market) Killing,” Wall Street Journal, April 23, 2010.

Karin Strohecker, “Global Debt Hits Record of Near $353 Trillion, with Signs of Move Away from U.S.,” Yahoo! Finance, May 6, 2026.

Financial Services Agency (FSA), “Cabinet Office Order Partially Amending the Cabinet Office Order on Electronic Payment Instruments, Etc.: Promulgation and Results of Public Comments,” May 19, 2026.

If one were to own a US Treasury ETF...like a BIL or longer duration, would these still be considered onshore USD as they are under US regulatory control, while not yet associated with stablecoins? Would you expect that the custodians themselves will manage the transition on behalf of these ETFs, rather than every individual needing to make this swap...whenever.